How To Clear Credit Card Payment

How to Clear Credit Card Debt Quickly in 2021

Many consumers are now seeking advice about the best ways to clear credit card debt after incomes have been slashed and balances have risen due to COVID-19. Credit card relief was being offered by credit card companies directly, including deferment of payments, fee waivers, and reduced interest rates, but this debt relief is coming to an end.

On the other hand, some folks may have some extra money that they want to use to pay off high-interest credit cards but need a better solution than what they're currently doing. Or perhaps, you're expecting some extra funds to come your way and don't know if you should invest the money in the stock market or pay off your high-interest credit cards. For example, the Child Tax Credit for 2021, an extension of the American Rescue Plan, is paying a tax relief payment of up to $3,000 for each child between 6 and 17 years old and up to $3,600 for every child under six years old.

Consequently, Golden Financial Services created the following credit card relief guide, highlighting the "Ten Best Ways to Clear Credit Card Debt." Of course, the best option for you will depend on the details of your financial situation. Credit card debt solutions range from methods that people can do on their own to debt relief programs.

So without further ado, here are the ten best ways to get out of credit card debt in 2021.

Debt counselors are also available to assist consumers with over $10,000 in credit card balances and are interested in learning about the programs available—Call 866-376-9846 for a Free Consultation Today.

How can I clear my credit card debt fast? The rest of this blog post provides a more detailed analysis of each option explained above in the info-graphic.

Even the rich and famous have credit card debt. Renowned musician, David Cassidy, had over $300,000 in credit card debt. Actor Stephen Baldwin owed over $70,000 in credit cards, according to a federal court filing. When Bernie Sanders and Ted Cruz were required to file financial disclosures for the presidential race many years back, it was revealed that they both owed above $60,000 in credit card debt. So, if you have found yourself struggling to pay off large credit card bills, know – you're not alone.

Table of Contents

- 1. Debt Snowball Method

- 2. Debt Avalanche

- 3. Balance Transfer Cards

- 4. Home Equity Line of Credit

- 5. How to Negotiate With Bank

- 6. Credit Card Hardship Program with Bank

- 7. Debt Validation

- 8. Debt Settlement

- 9. Consumer Credit Counseling

- 10. Bankruptcy

1. Debt Snowball Method:

The debt snowball method is the best way to get out of credit card debt for anyone who can comfortably pay more than minimum payments.

The debt snowball method, created by Dave Ramsey, is when you pay minimum payments on all of your credit cards besides the one with the smallest balance. Then, you're going to aggressively attack that smallest debt first by putting all of your extra money towards paying it off as fast as possible.

We go after the small debt first because that's where we will get the quickest result. And quick is the name of the game here. After each debt is paid in full, your available cash flow will continue to grow, just like when you're rolling a snowball. Your momentum will also continue to grow as your ball of cash increases in size, and you direct that ball of cash towards paying off the next debt in line.

After the smallest debt gets cleared away, shift your attention to the next smallest debt in line. One by one, you will continue to knock off each debt, getting closer and closer to the finish line.

Start by creating your budget with this free calculator here.

A budget will provide you with a visual image of where your money is going, making it easier to find non-essential expenses that can be reduced or eliminated. (example: lower the electric and heat bill, use coupons when shopping to save money at the grocery store, remove the HBO you never watch, and cancel that old subscription that you forgot was billing you each month).

You can then use this snowball calculator tool to figure out how long it will take you to become debt-free. The debt snowball calculator does all of the work. Just enter each debt you want to include in the snowball plan, and let the calculator work its magic. You can then download the information or save it; however, you choose and follow the plan.

Why Does the Debt Snowball Method Work?

Dave Ramsey explains: "The debt snowball works because it's all aboutbehavior modification, not math. When it all boils down, hope has more to do with this equation than math ever will. If you start paying on the student loan first because it's the largest account, it could take you years to get rid of that first debt. You'll see numbers going down on the balance, but pretty soon, you'll lose steam and stop paying extra. Why? Because it's taking forever to get a win! And you'll still have all your other small, annoying debts hanging around too."

Click Here to Use the Budget & Snowball Calculator

One last tip to avoid a big mistake:

Keep your credit card accounts open after paying off the balances so that your credit score improves. If you close a credit card account, your credit score will decline because your credit utilization ratio will be negatively affected.

2. The Debt Avalanche

The debt avalanche method is the best way to pay off high-interest credit card debt and reduce your monthly interest fees, according to Andrea Cannon from Wisebread.com.

The debt avalanche method is similar to the debt snowball method, but the difference with the debt avalanche is that you order your debts by their interest rate. So instead of paying off your smallest balance first, you would pay off the credit card balance with the highest interest rate first, the one costing you the most.

By paying off your most expensive accounts first, you can get out of debt faster and maximize your savings.

You may decide to use a combination of the debt snowball and avalanche method. For example, start by using the snowball method to pay off all of your balances under $1,000, then switch to prioritizing your debts by the interest rate and using the debt avalanche method. By going this route, you'll get to experience some quick wins, motivating you to continue, but also get to maximize your savings a bit more than just using the snowball method all along.

NerdWallet.com offers an excellent Debt avalanche calculator tool to help you get out of debt faster.

3. Pay Off Credit Card Debt With a Balance Transfer Card:

"Low Rate Balance Transfers | 0% Intro APR. Apply Now!"Wow, that's enticing until you read the fine print; "after 12-18 months, the introductory rate comes to an end, and the interest rate rises to 19.9%." Balance transfer cards also come with up-front fees. These fees range from 3%-5% of the amount of credit card debt getting transferred. If you move $10,000 onto a balance transfer card that charges a 4% fee, that's $400 in up-front costs.

Banks use balance transfer cards as a trap. They charge you the upfront fee for the card, and when you can't pay off your entire balance within the introduction-rate period, they jack up the interest rates. They make money when clients fail to pay off the balance within the intro period. They want you to fail.

When is a balance transfer card worth it?

- If you can afford to pay the balance "in full" within the 12-18-month introductory period, you could end up paying low to no interest and only a $400 fee. Shop around for a balance transfer card that comes with low costs and only go this route if you can afford to pay the balance in full within the introductory rate period. Use this debt national calculator tool to help you do the math.

- Choose a balance transfer card that pays you cashback. Bank of America offers a credit card that pays up to 3% cashback. For example, if you transfer $50K in credit card debt onto a balance transfer card that pays you 3%, you'll get reimbursed $1,500 in cash back. Put that $1,500 towards paying off your next credit card debt in line as you continue with the debt snowball method. You can eliminate 100% of interest and earn cash back when using a balance transfer card to pay off high-interest credit card debt.

Final Tip to Improve Your Credit Score

Keep your credit card accounts open after paying off the balances to keep your credit utilization ratio favorable.

4. Home Equity Line of Credit:

When using a home equity line of credit to pay off credit card debt, you're taking on considerable risk. This is because you're swapping unsecured debt for secured debt. If, for whatever reason, you can't afford to continue paying your scheduled monthly payments on the home equity line of credit, you could end up losing your home over a credit card debt, wherein you see the risk.

However, this is still one of my favorite tools for clearing credit card debt. The value of using a home equity line of credit to pay off credit card debt is that you're eliminating high-interest credit cards and replacing them with a low-cost home equity line of credit.

According to Bankrate.com, 5.56% is the average interest rate on a home equity line of credit as of May 2018, significantly lower than the average interest rate on a credit card.

5. How to Negotiate With a Bank to Reduce the Interest Rate

Try negotiating directly with your creditor to reduce the interest rate and monthly payment. In many cases, all it takes is a simple and quick phone call. You may even be able to convince a creditor to lower your interest rate permanently.

Here's a simple script that you can use to negotiate with your creditor.

Call your creditor and ask to speak with a Supervisor because only a Supervisor will have the authority to make these changes. Say the following:

"Hello ____, how are you today? I've been a loyal client for ___ years now and have always paid my bills on time, so I hope you can help me today so that I can keep my credit card account open with your bank. Your hands may be tied, and you may not have any power to help me here, but I figured I'd try to openly communicate with you about this matter before just closing my card. I want to stay with your bank as you guys have always been good to me. Anyway, here's my situation; _______ bank offered me a ___% interest rate on a similar card with 3% cashback included. Since this interest rate is ___% less than what your card is offering me, I've decided to close this card out and switch to the new card that ____ bank is offering me. Unless, of course, you can reduce my interest rate or upgrade my card to match what _____ bank is offering and offer me some similar cashback. What do you have the power to offer me today to help me out? " Then go silent.

6. Credit Card Hardship Program with Bank (e.g., Chase, Bank of America & Citi)

In some cases, you may only be able to get a temporary reduction in the monthly payment, but if you're going through financial hardship (like many consumers are due to COVID-19), that may be your best solution.

To be considered for a bank's credit card hardship program, you must be behind on your monthly payment, but not to the point where your credit report is negatively affected. Some banks may have also extended COVID-19 debt-relief options but only consider one of these plans if the creditor is willing to pause the interest and payment. Otherwise, the interest continues accruing and just gets tacked on to your existing balance, making your debt grow even larger. Credit card forbearance and deferment options are only worth considering if the interest is either reduced or paused.

Steps to get approved for your bank's credit card hardship program without a negative effect on credit scores

- The trick is to call your creditor in 7-10 days after you miss the monthly payment. Unfortunately, late payment history doesn't get reported to the credit reporting agencies until you're more than 29 days past due.

- To strengthen your case, send the creditor a copy of your budget analysis, a financial hardship letter, and evidence to validate your reason for needing a lower payment before calling them.

- When calling your creditor, request to speak to a supervisor because they have the authority to reduce your monthly payment. Let the supervisor know that you're calling to see if they can temporarily lower your monthly payment. Go over the fact that you could not afford to make your last monthly payment and explain why. Include the details of your financial hardship. Make sure to keep your story in line with what you stated in the hardship letter. Also, reassure your creditor that your financial hardship is only temporary and provide an estimate for how long you'll need the relief.

- The supervisor will ask you a series of questions about your income. At that point, verify that they received your budget analysis, hardship letter, and whatever documentation you sent. Then, use this free budget calculator to create your budget.

You'll be rejected from a bank's credit card hardship program if your income is too low due to insufficient income. On the other hand, if your income is too high, they may not consider you to have a real financial hardship. There is no set number, but as a general rule of thumb, consider showing that you could reasonably afford about half of the projected monthly payment that is currently required.

7. Debt Validation Plans Last For Three Years (average)

How can I get out of debt without paying? This next option is your closest route to getting out of credit card debt without paying. After credit card collection accounts are invalidated, legally, they no longer need to get paid.

Before signing up for a debt settlement/negotiation program, consider debt validation. The programs available at Golden Financial Services will only attempt to negotiate and settle a credit card debt after it's proven to be valid.

Debt validation can't magically erase your debt, but it can be the most effective and least expensive route to dealing with unsecured debt and negative credit. For this reason, we've put debt validation above debt settlement and consumer credit counseling plans.

Why debt validation over debt settlement services?

- Pay less than what you would pay if settling a debt

- After a debt is proven to be legally uncollectible, it can no longer legally remain on credit reports

- The average plan is for 36 months, versus 42+months on settlement

- No taxes owed if a debt is proven to be invalid

- Money-back guarantee

- Accounts can sit for over a year before they are negotiated, leaving more time for lawsuits to occur with settlement services. Third-party collection agencies, including Midland Funding, Portfolio Recovery, and Cavalry Portfolio, are issuing lawsuits in under sixty days after receiving credit card accounts, resulting in debt settlement programs becoming much costlier because settlements are no longer attractive. Debt validation can get in front of this change, in many cases disputing the debt before lawsuits occur.

The New York Times recently reported; major banks like American Express, Citigroup, Bank of America, Capital One, and Chase

- committed fraud in business dealings

- are using erroneous paperwork

- have incomplete records

- use faulty legal processes

Noach Dear, a New York Supreme Court Judge, estimated that 90% of credit card lawsuits are flawed and can't prove the person owes the debt.

Possible Reasons for Why a Debt Could Become Invalidated

- Unauthorized fees get added in, making it impossible for a collection agency to prove the debt is valid.

- The collection agency may not produce a valid debt collector's license for a particular state.

- Paperwork gets lost or missing documentation, like a collection agency may not produce the original agreement signed when the consumer first applied for the credit card.

- Incomplete records get transferred from the original creditor to the collection agency.

- The statute of limitations on a debt may have expired, or collection agencies can't supply accurate information about when the statute of limitations is set to expire. Remember, for an account to be "valid," it must be legally verifiable with complete and accurate records after being requested.

- To expand on this last point, a collection agency may not be able to produce accurate information about the date the statute of limitations on a credit card account expires, the full account number on a credit card when it was with the original creditor, the date the credit card account was sold to a third-party collection agency, the debtor's personal information including date of birth, mailing address and social, and much more.

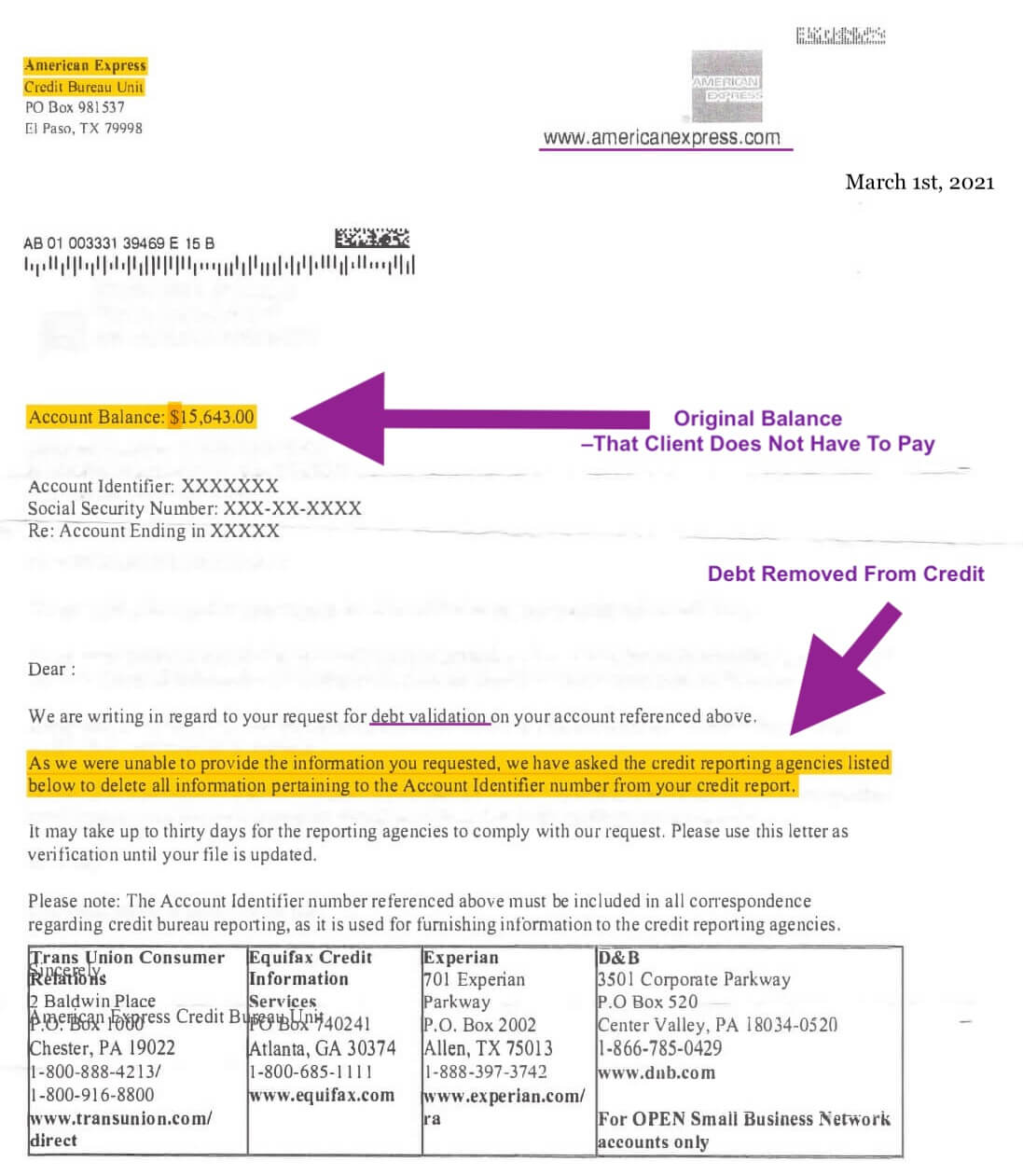

In many cases, after a debt is disputed with debt validation, a collection agency will quickly respond with a letter agreeing to stop collection on the debt. The reason that collection agencies so quickly agree to stop collection on a debt after it's disputed is often unknown. It varies, but the outcome is always the same – if a collection agency can't prove an account is valid, it becomes legally uncollectible, and you don't have to pay it. Therefore, the following letter acts as a defensible record proving the debt to be invalid. Here is an example of the letter:

American Express (Debt Collection): $15K+Balance Does Not Have To Be Paid & Comes Off Credit Reports.

Do your creditors get paid?

In the example above, the collection agency agrees to stop collection on this debt for over $15,000, but rest assured the original creditor was paid back in full.

First off, the original creditor will write off the debt showing it as a loss, reimbursing 100% of the money through tax credits.

Secondly, the original creditor profits by selling the credit card account to a collection agency. More profit!

Thirdly, credit card companies can get reimbursed through banking insurance. Like how people have car insurance, banks have banking insurance.

And fourthly, consider all of the late fees and interest that accrue after the borrower stops paying on a credit card, artificially inflating the balance even more, and banks will eventually write all of it off. So, in the end, banks may get paid back more than three times what was owed on the original credit card balance.

Since banks are reimbursed all of the money owed on an unpaid credit card balance and sometimes more explained, they get careless when selling delinquent credit card accounts to collection agencies. In summary, paperwork goes missing, and information turns inaccurate.

Consequently, consumers benefit by using debt validation and consumer protection laws to dispute a debt.

What if a debt is proven to be valid, or you get sued?

There is a small chance that a client receives a summons on a debt after joining any debt settlement or validation program. No matter what program or company a person uses, there's always the chance of this happening.

If a summons is received while enrolled on the validation program offered through Golden Financial Services, the consumer is immediately refunded on that account and referred to a settlement law firm that will settle the debt for less than the full amount owed. Thus, the summons becomes a priority and gets resolved right away.

Clients are educated on what to do if they receive a summons at the beginning of their program, so there are never any surprises. For that reason, Golden Financial Services has had no complaints over the last three years and maintains a very positive reputation online, along with an A+BBB rating since 2004.

Contact Golden Financial Services for a free consultation today at (866) 376-9846.

Debt Relief Program Info-graphic (Pros vs. Cons)

8. Debt Settlement Services to Get Out Of Credit Card Debt in Under Four Years

If you can't afford to stay current on your credit card payments, debt settlement can reduce the balances and allow you to clear credit card debt in around three to four years.

Let's look at an example:

A debt settlement program could resolve $50,000 worth of credit card debt for $30,602. When paid over three years, that would result in a monthly payment of $850.

Versus:

When paying minimum payments on $50,000 of credit card debt, the monthly payment would be around $1,400, and it could take approximately six years or longer to pay the debt off in full (depending on the interest rate).

As you can see, debt settlement programs can offer a much lower monthly payment for consumers struggling to pay their credit cards.

Additionally, you can avoid bankruptcy.

Try this debt calculator to see your options:

Negative consequences of debt settlement include:

- Credit scores go down, and derogatory notations will appear on credit due to creditors not getting paid every month (including late and collection marks).

- There is no guarantee that a creditor will settle at a certain percentage.

- The IRS could require a person to pay taxes on the amount saved after a credit card settlement.

- Late fees and interest can cause balances to increase over the first year of the program.

- A creditor could issue a person a summons to go to court, and although this is rare, it could happen.

Contact Golden Financial Services Today, and We Can Help You Get Approved For the Lowest Possible Payment. (866) 376-9846

9. Consumer Credit Counseling to Pay Off Credit Cards in Less Than Five Years

If you can't pay off credit card balances due to high-interest rates, consumer credit counseling could be your best solution.

A consumer credit counseling (CCC) plan, also known as credit card consolidation, may lead to lower interest rates and the consolidation of several of your monthly payments into an easier to deal with, more manageable single payment.

It's common to see 25% interest rates get reduced to 8%-10%. In addition, consumer credit counseling can lead a person out of credit card debt within 4-5 years versus 9-15 years when paying minimum payments.

Although participation in CCC has a minimal effect on a person's credit score, there may be some adverse consequences to consider.

For example, anytime you change the original terms on your credit card contract, your credit rating has an adverse effect. And with consumer credit counseling, a third-party notation gets reported on your credit report. Lastly, credit cards are closed out after joining a consumer credit counseling program, resulting in a negative effect on credit scores.

The good news is that with consumer credit counseling, you don't have to fall behind on payments, like with debt validation and settlement programs.

Why would a person choose consumer credit counseling over debt settlement or validation?

Depending on what your goal is will determine what program is best for you.

If your primary goal is to get the lowest possible payment and be done with the program in the quickest time frame, debt settlement and validation will surely be more appealing.

If you have a 750 credit score and have no late marks on your credit, your goal may be to preserve that perfect credit history.

Even though you can save more with debt settlement or validation, you may decide it's not worth having to deal with the stress that comes along with debt settlement, about late and collection marks on credit, and the possibility of getting sued.

You have to consider the pros and cons of each option and weigh the benefits versus downsides side by side.

When it comes to financial hardship plans like settlement and validation, you need to be mentally strong and see the big picture and be ready to stick to the plan no matter how stressful things may get. A reputable debt relief company is experienced in helping its clients get through a hardship program no matter what happens. If they get sued, the company is aligned with attorneys ready to resolve a summons.

10. Chapter 7 Bankruptcy Can Clear Credit Card Debt in Under 6 Months

Why is Chapter 7 the preferred way of bankruptcy?

The reason is that Chapter 7 bankruptcy wipes away credit card debt so that it doesn't have to get paid.

Chapter 7 bankruptcy only lasts for 3-6 months, making this one of the fastest ways to clear credit card debt in 2021.

With chapter 7 bankruptcy (also known as "liquidation bankruptcy"), a debtor's assets are sold, and the proceeds are used to pay off creditors. However, 95% of debtors do a "no asset filing" because they don't have any assets to be sold. If a debtor doesn't have any assets to get sold, their debts are discharged and no longer legally owed.

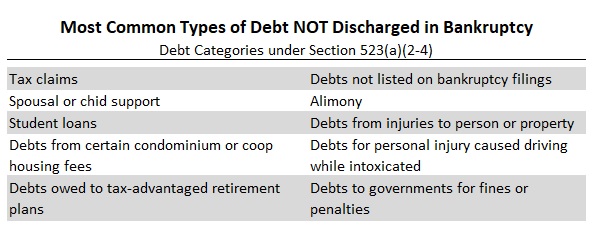

Credit cards, private student loans, medical bills, and almost all unsecured debts can get discharged and wiped away clean (excluding federal student loans, tax claims, spousal or child support, condominium and housing fees, alimony, and a few others).

Debts NOT Discharged in Chapter 7 Bankruptcy

The Downsides of Bankruptcy:

- Your credit score can get lowered by 175 points.

- Next to each creditor that gets discharged, it will say, "debt discharged due to bankruptcy."

- Potential employers, landlords, and creditors will all be able to see that you filed for bankruptcy.

- Credit scores will be subprime after filing for bankruptcy, making it difficult to get approved for low-interest rates on any credit.

- Premiums on car insurance, cell phone, and monthly insurance payments can all legally increase once bankruptcy goes on a person's credit report.

- Chapter 7 bankruptcy can stay on your credit report for 10-years

Here's a bankruptcy guide to help you learn more about bankruptcy if this is an option you're seriously considering.

About the author:

Paul J Paquin is the CEO of Golden Financial Services, a national debt relief company specializing in helping consumers achieve financial freedom and credit card relief. Paul integrates his experiences and insights from Golden Financial Services into his writing, sharing solutions to Americans' everyday financial challenges. Paul's passionate about empowering consumers with the knowledge needed to improve their finances and take control of debt. He's created numerous guides on debt-related subjects; a few of the most popular include "A Guide to Understanding Unsecured vs. Secured Debt" and "The Ultimate Guide on How to Get Student Loan Forgiveness."

How To Clear Credit Card Payment

Source: https://goldenfs.org/best-ways-to-clear-high-credit-card-debt/

Posted by: baldwinbusert1997.blogspot.com

0 Response to "How To Clear Credit Card Payment"

Post a Comment